Tariff on, Tariff off

4/8/20259 min read

Analysis of Trump's 2025 Tariff Policy and its Potential Impact on the US Economy and Financial System

Executive Summary

In early April 2025, President Trump enacted a significant new tariff policy, marked by a baseline 10% tariff on imports from nearly all countries and higher, "reciprocal" tariffs targeting nations with substantial trade deficits with the United States.1 This policy is anticipated to generate negative repercussions for the US economy, with projections indicating reductions in GDP and wages, alongside increases in costs for American households.3 The financial system is also expected to face disruptions, evidenced by initial stock market volatility and potential complications for the Federal Reserve's monetary policy as inflationary pressures are likely to mount.3 Furthermore, the international community has responded with retaliatory tariffs from major trading partners, posing a considerable threat to the stability of global trade.8 Historical parallels with past US tariff policies, notably the Smoot-Hawley Tariff Act, suggest the potential for adverse economic outcomes stemming from this protectionist approach.1 The swift implementation and extensive scope of these tariffs represent a notable shift in trade strategy, potentially delivering an abrupt shock to the global economic landscape.1

Introduction: Context and Genesis of the 2025 Tariff Policy

President Trump has consistently advocated for the use of tariffs as a primary instrument to safeguard domestic industries and diminish trade deficits, a stance evident throughout his previous term and reiterated during his campaign.13 This commitment materialized in a series of announcements and executive orders leading up to the comprehensive tariff policy unveiled in April 2025. The timeline began in January 2025 with his inaugural address, where he reaffirmed his intention to implement tariffs.13 February saw the signing of an executive order imposing tariffs on imports from Mexico, Canada, and China, citing a national emergency related to immigration and drug trafficking. This period also included announcements regarding planned tariffs on steel, aluminum, and the concept of "reciprocal" tariffs.9 In March 2025, further details emerged concerning tariffs on steel, aluminum, and automobiles.9 The culmination of these efforts occurred on April 2, 2025, with the announcement of the "reciprocal" tariff policy. This included a baseline 10% tariff on nearly all imports and higher tariffs on specific countries identified as having the largest trade surpluses with the US. This announcement was accompanied by a declaration of a national emergency predicated on the persistent US trade deficit.1

The stated objectives underpinning this tariff policy are multifaceted. A primary goal is the reduction of the US trade deficit, which exceeded $1.2 trillion in 2024.8 The administration also aims to protect American workers and industries by creating incentives for domestic production, a process often referred to as "re-shoring".8 Addressing what are perceived as "unfair" trade practices and existing tariff disparities imposed by other nations is another key motivation.8 Finally, the policy seeks to bolster national and economic security by lessening the reliance on foreign supply chains for critical goods.8 The decision to invoke "national emergency" under the International Emergency Economic Powers Act (IEEPA) to justify the imposition of these tariffs underscores a strategic utilization of executive authority. This approach potentially circumvents traditional Congressional oversight in the realm of trade policy, allowing for a more expedited implementation.1

Detailed Examination of the Tariff Structure

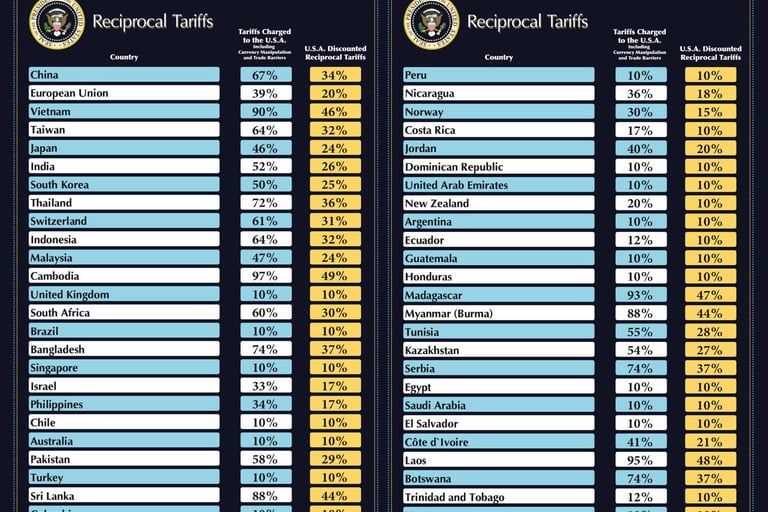

The tariff policy as of April 2025 comprises several key elements. A baseline tariff of 10% ad valorem was applied to imports from nearly all countries, taking effect on April 5, 2025.1 In addition to this, reciprocal higher tariffs, ranging from 11% to 50% initially, were slated for imports from countries with the largest trade deficits with the US, effective April 9, 2025.1 However, these higher reciprocal tariffs (above the 10% baseline) were temporarily suspended for 90 days for all countries except China, starting on April 10, 2025.1 It is crucial to note that these new tariffs are layered on top of existing tariffs on steel (25%), aluminum (25%), and automobiles (25%), which were implemented earlier.2 Goods compliant with the USMCA generally maintain a 0% tariff, although exceptions exist for non-compliant goods, energy, and potash from Canada and Mexico.2 Certain product exemptions may apply to goods like bullion, energy and minerals not found domestically, and potentially semiconductors, pharmaceuticals, copper, and lumber, although these remain subject to further investigations.2 Notably, China faces a significantly elevated tariff burden, encompassing the baseline 10% plus additional tariffs, culminating in a total of 125% after accounting for retaliation and counter-retaliation. Furthermore, the de minimis exemption for goods from China was revoked.1

The multi-layered and frequently changing nature of this tariff structure, involving baseline rates, country-specific adjustments, temporary suspensions, pre-existing tariffs, and product exemptions, introduces substantial uncertainty for businesses engaged in international trade. This ambiguity can impede investment decisions and complicate long-term strategic planning.1

Table 1: Summary of Key Trump Administration Tariffs (April 2025)

Projected Macroeconomic Effects on the US Economy

Economic models project a substantial contraction in economic activity as a consequence of these tariffs. The Penn Wharton Budget Model anticipates a long-run reduction in GDP of approximately 6%.3 J.P. Morgan Research estimates a potential 1% decrease in global GDP resulting from a 10% universal tariff combined with higher tariffs on China.22 The Yale Budget Lab forecasts a 1.1 percentage point decline in US real GDP growth due to all tariffs implemented in 2025.23 This convergence of findings across different economic models suggests that the broader economic costs associated with the tariffs may outweigh the intended benefits of protecting domestic industries.3

The impact on employment and wages is also projected to be negative. The Penn Wharton Budget Model predicts a long-run wage reduction of about 5%.3 The Yale Budget Lab foresees a 0.55 percentage point increase in the unemployment rate and a reduction of 740,000 payroll jobs by the end of 2025.23 Notably, studies examining the 2018-2019 tariffs indicated that they failed to stimulate employment and instead harmed the manufacturing sector due to increased input costs and retaliatory measures.24 The anticipated negative effects on wages and employment contradict the stated objective of the tariffs to safeguard American workers. It suggests that higher costs and decreased demand may lead to job losses rather than job creation.3

Furthermore, the tariffs are expected to exert significant inflationary pressure, as they function as a tax on imported goods, thereby increasing consumer prices.20 The Yale Budget Lab estimates a short-run increase in the overall price level of 2.9%, translating to an average household consumer loss of $4,700 annually.23 The Boston Fed projects that the proposed tariffs could add between 0.5 and 0.8 percentage points to core inflation.27 These rising prices will likely diminish consumer purchasing power, potentially leading to a slowdown in consumer spending growth, despite an initial period where consumers might frontload purchases to avoid anticipated price hikes.20 It is also anticipated that low-earning families will experience the most significant negative impact from these tariffs.4

Impact on the US Financial System

The immediate reaction of financial markets to the announcement of the tariff policy on April 2, 2025, was negative, with a global sell-off occurring in both equities and US Treasuries, causing a decline in financial markets worldwide.2 However, the subsequent announcement of a 90-day pause on most of the additional tariffs above 10% triggered a rebound in stock markets.2 The lack of clarity surrounding the specifics of the tariffs also contributed to broader economic volatility and the initial stages of a stock market downturn in 2025.1 This initial negative reaction underscores investor concerns regarding the potential adverse effects of the tariffs on corporate earnings, economic growth, and the stability of global trade.1 The subsequent market recovery upon the announcement of a pause suggests that the financial system is sensitive to shifts in trade policy and generally favors a less protectionist stance.

In the longer term, the uncertainty surrounding the final framework of the tariffs could continue to negatively affect consumer and business sentiment, potentially leading to further market volatility.20 Concerns about rising inflation, driven by the tariffs, could also put upward pressure on bond yields as investors demand greater compensation for the anticipated erosion of their purchasing power.3 Furthermore, a significant deceleration in GDP growth as a result of the tariffs could negatively impact corporate earnings, potentially leading to a decline in stock valuations.3 The ultimate long-term impact on the financial system will likely hinge on the duration and scope of the tariffs, the responses from international trading partners, and the policy decisions made by the Federal Reserve. Persistent uncertainty and negative economic consequences could result in a sustained period of market instability and potentially lower asset values.1

The Federal Reserve's Response and Policy Implications

The implementation of these tariffs presents a complex challenge for the Federal Reserve as it navigates its dual mandate of maintaining price stability and maximizing employment.6 The tariffs are likely to generate inflationary pressures, which could impede the Federal Reserve's ability to consider interest rate cuts that might otherwise be warranted.5 Federal Reserve Chair Jerome Powell has acknowledged the potential for the tariffs to lead to both increased inflation and a slowdown in economic growth, a condition known as stagflation, which would create significant difficulties for monetary policy.1

In response to this uncertainty, the Federal Reserve may adopt a cautious, "wait-and-see" approach to thoroughly assess the actual impact of the tariffs on both inflation and employment before implementing any substantial policy adjustments.6 Should the tariffs trigger a significant economic downturn accompanied by a rise in unemployment, the central bank might feel compelled to lower interest rates to stimulate economic activity, even if inflation remains at an elevated level.6 Conversely, if the tariffs result in a sustained increase in inflation without a corresponding significant rise in unemployment, the Federal Reserve might need to consider raising interest rates to curb price pressures, potentially further hindering economic growth.6 The imposition of broad tariffs creates a considerable dilemma for the Federal Reserve, as the potential for both rising inflation and slowing economic growth could put its dual mandate in conflict, making it considerably more challenging to determine the appropriate course for monetary policy. The uncertainty introduced by these trade measures is likely to lead to a more data-dependent and cautious stance from the central bank.6

International Repercussions and Trade Relations

The response from major US trading partners to the imposition of these tariffs has been swift and indicative of potential escalating trade disputes. China immediately retaliated by imposing tariffs on a range of US goods and initiating an anti-monopoly investigation into Google.9 These retaliatory tariffs from China were subsequently increased in response to further US tariff hikes, eventually reaching a cumulative total of 125%.10 Canada and Mexico also announced and implemented their own retaliatory tariffs on US goods, including automobiles.9 The European Union initially announced retaliatory tariffs on US goods in response to tariffs on steel and aluminum but later decided to pause these measures.2 Colombia initially announced retaliatory tariffs but subsequently reversed this decision.13

These prompt and significant retaliatory actions from major trading partners highlight the deeply interconnected nature of the global economy and the high likelihood of escalating trade disputes as a consequence of unilateral tariff measures. This unfolding "trade war" scenario has the potential to negatively impact businesses and consumers in all involved countries.2 In the long term, these tariffs could lead to a fragmentation of existing global supply chains as businesses seek to diversify their production sources to mitigate the impact of tariffs.8 Furthermore, the erosion of WTO commitments and the increasing trend towards unilateral trade actions could undermine the established rules-based international trading system.14 The heightened trade tensions also carry the risk of straining diplomatic relationships with key allies and trading partners.31 This shift towards protectionism, as evidenced by these tariffs, could have enduring negative consequences for the global trading system, potentially resulting in reduced efficiency, higher costs, and increased geopolitical friction.14

Historical Perspective: Lessons from Past US Tariff Policies

A significant historical parallel can be drawn with the Smoot-Hawley Tariff Act of 1930 and its subsequent economic ramifications.1 The Smoot-Hawley Act significantly increased tariff rates on a wide range of imported goods and is widely regarded as having exacerbated the Great Depression due to the retaliatory tariffs it provoked from other countries, leading to a sharp contraction in global trade.11 Notably, the current average effective US tariff rate is estimated to be at its highest level since the era of the Smoot-Hawley Act.1 Similar to the present situation, economists at the time issued warnings against the potential negative consequences of the Smoot-Hawley Act.12 The historical precedent of the Smoot-Hawley Tariff Act serves as a stark reminder of the potential for protectionist trade policies to trigger adverse economic outcomes, including trade wars and economic downturns. The similarities in the scale and scope of the current tariffs raise significant concerns among economists about the possibility of repeating past policy missteps.1

Beyond the Smoot-Hawley Act, other historical examples of US tariff policies offer insights. In the 19th century, tariffs served as a primary source of revenue for the federal government but also contributed to regional economic tensions.11 These historical instances underscore the dual nature of tariffs, capable of generating revenue and protecting domestic industries but also carrying the risk of unintended negative consequences.

Conclusion: Navigating the Uncertainties of the New Tariff Regime

The analysis indicates that President Trump's recent tariff policy carries significant potential for negative impacts on the US economy and financial system. The projected reductions in GDP and wages, coupled with the anticipated rise in inflation and the potential for disruptions in financial markets, paint a concerning picture. The swift retaliatory actions from major trading partners further underscore the risks associated with this protectionist approach. The historical parallels with the Smoot-Hawley Tariff Act serve as a stark warning about the potential for such policies to exacerbate economic difficulties.

The long-term effects of this tariff regime remain highly uncertain, particularly given the temporary suspension of some tariffs and the ongoing threat of further escalations in trade tensions. Businesses, consumers, and policymakers, including the Federal Reserve, face considerable challenges in navigating this ambiguous economic landscape. The ultimate success or failure of this policy will depend on a multitude of factors, including the responses of global trading partners, the underlying resilience of the US economy, and any future adjustments or reversals in the policy itself. Ultimately, the resurgence of protectionist trade policies poses considerable risks to global economic stability. The temporary pauses and the threat of further escalations create a highly uncertain economic environment for businesses and investors, making informed decision-making exceptionally difficult.1 Monitoring the reactions of international partners and the future trajectory of the policy will be crucial in understanding its long-term consequences.