Nvidia: Navigating the AI Revolution

Our analysis of Nvidia's Q4 FY2025 earnings leads to a Buy rating, driven by their commanding position in the burgeoning AI and data center markets. The company exceeded expectations with strong revenue and EPS growth, fueled by the successful launch of the Blackwell architecture. We anticipate continued robust performance, particularly within the Data Center and Automotive segments. While acknowledging potential short-term margin pressures and increasing competition, Nvidia's technological leadership and strategic partnerships position them for sustained growth. Overall, we view Nvidia as a compelling investment opportunity within the evolving technology landscape.

3/8/202515 min read

Nvidia: Navigating the AI Revolution

1. Executive Summary:

This report provides an equity research analysis of Nvidia Corporation (NVDA) following its latest earnings release on February 26, 2025. Our analysis indicates a compelling investment opportunity, leading to a Buy rating. We believe Nvidia stands at the forefront of the artificial intelligence revolution, holding a dominant position in the rapidly expanding AI and data center markets, which is further strengthened by the successful launch of its Blackwell architecture. The company's financial performance in the fourth quarter of fiscal year 2025 exceeded analyst expectations in both revenue and earnings per share, and its revenue guidance for the first quarter of fiscal year 2026 is robust. While there are potential short-term margin pressures associated with the Blackwell ramp-up and increasing long-term competition, we believe the overall outlook for Nvidia remains bullish. This positive perspective is driven by the sustained and growing demand for its AI solutions and its leadership in critical technology sectors.

2. Company Overview:

Founded in 1993, Nvidia has undergone a significant transformation from a graphics card manufacturer to a pivotal technology company at the heart of accelerated computing and artificial intelligence. The company's fundamental expertise lies in the design and production of graphics processing units (GPUs), systems-on-a-chip (SoCs), and associated software platforms 1. Nvidia operates through several key business segments, each contributing to its overall performance and growth trajectory.

The Gaming segment primarily focuses on GeForce GPUs designed for desktop and laptop personal computers, as well as the GeForce NOW cloud gaming service. In the fourth quarter of fiscal year 2025, this segment generated $2.5 billion in revenue, marking an 11% decrease year-over-year and a 22% sequential decline 1. However, for the full fiscal year 2025, the Gaming segment achieved revenue of $11.4 billion, representing a 9% increase compared to the previous year 1. We note that the revenue decrease in the latest quarter was largely due to supply constraints affecting both the current Ada Lovelace architecture and the newly introduced Blackwell architecture GPUs 1.

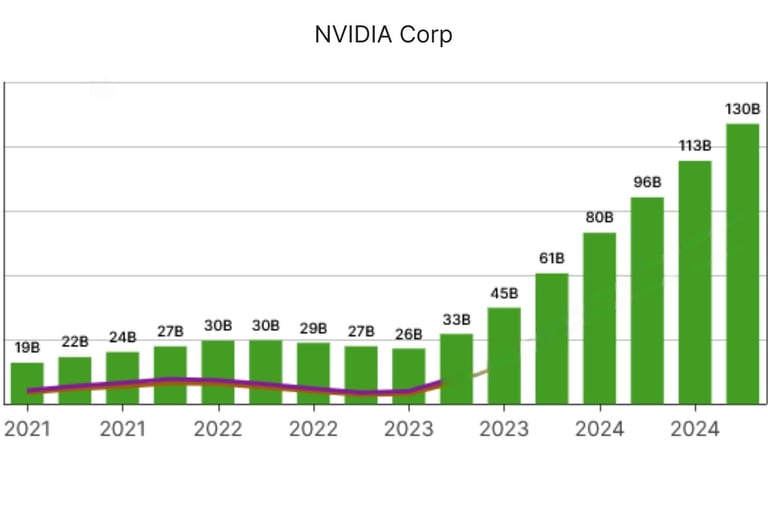

The Data Center segment has emerged as Nvidia's largest revenue contributor, offering high-performance GPUs and advanced networking solutions crucial for artificial intelligence, machine learning, high-performance computing, and cloud infrastructure. This segment achieved a record revenue of $35.6 billion in the fourth quarter of fiscal year 2025, demonstrating an impressive 93% year-over-year growth and a 16% sequential increase 1. For the entire fiscal year 2025, the Data Center segment's revenue soared to $115.2 billion, marking a remarkable 142% increase compared to the previous fiscal year 1. We believe this segment's performance underscores Nvidia's dominance in the AI infrastructure market.

The Professional Visualization segment provides Quadro GPUs and specialized software designed for professionals in fields such as design, engineering, media, and entertainment. In the fourth quarter of fiscal year 2025, this segment reported revenue of $511 million, indicating a growth of 10% year-over-year and 5% sequentially 1. The full-year revenue for fiscal year 2025 reached $1.9 billion, representing a 21% increase year-over-year 1. We view this as a steady growth segment, benefiting from the increasing complexity of professional workflows.

The Automotive segment focuses on the NVIDIA DRIVE platform, which offers solutions for autonomous vehicles, AI-powered in-car experiences, and other automotive applications. This segment achieved a record revenue of $570 million in the fourth quarter of fiscal year 2025, demonstrating substantial growth of 103% year-over-year and 27% sequentially 1. For the full fiscal year 2025, the Automotive segment's revenue was $1.7 billion, a significant 55% increase year-over-year 1. We are particularly optimistic about the long-term potential of this segment as autonomous driving technology matures.

The OEM and Other segment includes revenue generated from licensing intellectual property and other smaller business lines. In the fourth quarter of fiscal year 2025, this segment reported revenue of $126 million, showing strong growth of 40% year-over-year and 30% sequentially 3. The full-year revenue for fiscal year 2025 was $389 million, a 27% increase year-over-year 3.

Nvidia's diverse business segments are strategically positioned to capitalize on high-growth areas within the technology sector. The remarkable expansion of the Data Center segment highlights its critical role in the ongoing AI revolution, while the rapidly developing Automotive segment signifies a substantial long-term opportunity. The Gaming and Professional Visualization segments provide a consistent and expanding revenue base for the company. We believe the balanced contribution from these segments underscores Nvidia's adaptability and its capacity to leverage multiple technological advancements.

3. Recent Financial Performance (Q4 FY2025 Analysis):

3.1 Key Financial Metrics:

Nvidia's financial results for the fourth quarter of fiscal year 2025, which ended on January 26, 2025, demonstrated exceptional performance. The company reported revenue of $39.3 billion, which not only exceeded its own prior guidance of $37.5 billion (plus or minus 2%) but also surpassed the consensus analyst estimates that ranged from $38.1 billion to $38.32 billion 1. This figure represents a substantial year-over-year increase of 78% and a sequential growth of 12%. We view this significant beat as a testament to the strong demand for Nvidia's products.

In terms of profitability, Nvidia reported GAAP net income of $22.091 billion, up significantly from $12.285 billion in the same quarter of the previous year, representing an 80% year-over-year increase 1. Non-GAAP net income was $22.1 billion, a 72% increase compared to the $12.839 billion reported in the fourth quarter of fiscal year 2024 1. These figures highlight the company's strong earnings power.

GAAP earnings per share (EPS) reached $0.89, a remarkable 82% increase from the $0.49 reported in the prior year's fourth quarter, and it also beat analyst estimates of $0.85 1. Non-GAAP EPS also came in at $0.89, representing a 71% year-over-year growth from $0.52, and it exceeded the consensus estimates that ranged from $0.84 to $0.85 1. The EPS beat further reinforces our positive view on the company's profitability.

Looking ahead, Nvidia provided strong revenue guidance for the first quarter of fiscal year 2026, projecting approximately $43 billion, with a potential variation of plus or minus 2% 1. This outlook surpassed the average analyst consensus, which was around $42.11 billion to $43.37 billion 13. We believe this robust guidance indicates continued strong demand in the coming quarter.

3.2 Analysis of Earnings Beat/Miss and Revenue Surprise:

Nvidia has established a consistent track record of exceeding market expectations. The significant revenue surprise in Q4 FY2025, ranging from $1.0 billion to $1.19 billion, and the EPS surprise of $0.04 to $0.09 demonstrate the company's strong business momentum and its ability to capitalize on market opportunities 4. This pattern of outperforming analyst forecasts for both revenue and earnings per share over several consecutive quarters suggests a robust underlying demand for Nvidia's products and services, particularly in the rapidly expanding AI and data center markets 20. We believe this consistent ability to beat expectations likely contributes positively to investor confidence and market sentiment surrounding the stock.

3.3 Discussion of Gross Margins and Operating Expenses:

Despite the impressive revenue and earnings growth, both GAAP and non-GAAP gross margins experienced a slight contraction in the fourth quarter of fiscal year 2025. The GAAP gross margin was reported at 73.0%, a decrease of 3.0 percentage points compared to the same period in the previous year 1. The non-GAAP gross margin was 73.5%, representing a decline of 3.2 percentage points year-over-year 1. While the margin contraction is a point to note, we believe it is temporary.

The company attributed this margin compression primarily to the higher initial production costs associated with the ramp-up of its new Blackwell architecture and some temporary inefficiencies within the supply chain 7. Management has indicated that they anticipate gross margins to recover to the mid-70% range later in fiscal year 2026 as the production of Blackwell scales and operational efficiencies are realized 4. We concur with this assessment and expect margins to improve as Blackwell production matures.

Operating expenses also saw a significant increase in the fourth quarter. GAAP operating expenses rose by 48% year-over-year to $4.689 billion 1, while non-GAAP operating expenses increased by 53% year-over-year to $3.378 billion 1. This growth in operating expenses was primarily driven by higher compensation and benefits expenses due to an increase in employee headcount and compensation adjustments, as well as greater investments in engineering development, computing infrastructure, and infrastructure costs to support the introduction of new products 1. We believe these increased investments are necessary to support the company's rapid growth and maintain its technological edge.

4. Business Segment Performance:

4.1 Gaming:

The gaming segment experienced a decrease in revenue in Q4 FY2025, with a decline of 11% year-over-year and 22% sequentially, reaching $2.5 billion 1. This downturn was primarily attributed to supply constraints affecting both the current generation Ada Lovelace GPUs and the newly launched Blackwell architecture GPUs, despite robust demand during the holiday season 1. However, for the full fiscal year 2025, the gaming segment demonstrated resilience, achieving a 9% increase in revenue to $11.4 billion, driven by strong sales of the GeForce RTX 40 Series GPUs 1. Looking ahead, the introduction of the GeForce RTX 50 series GPUs, based on the Blackwell architecture, is anticipated to be a significant growth catalyst, offering substantial performance enhancements and integrating advanced AI-powered features such as DLSS 4 and Reflex 2 2. Despite the short-term challenges related to supply, we believe the underlying demand for Nvidia's gaming products remains solid, and the upcoming product cycle is expected to drive future growth in this segment.

4.2 Data Center:

The Data Center segment continued its exceptional growth trajectory, achieving a record revenue of $35.6 billion in Q4 FY2025, representing a remarkable 93% year-over-year increase and a 16% sequential growth 1. This growth was primarily driven by the sustained and increasing demand for Nvidia's accelerated computing platforms, which are essential for large language models, recommendation engines, and generative AI applications 1. A significant contributor to this performance was the successful launch and rapid adoption of the Blackwell architecture, which generated $11 billion in revenue in its first quarter, marking the fastest product ramp in the company's history 1. Demand for the previous generation Hopper GPUs also remained strong, particularly from major cloud service providers who are making substantial investments in AI infrastructure 2. The Q1 FY2026 revenue guidance for the Data Center segment, projected to be around $39.3 billion, further indicates the continued strong momentum in this critical market 4. Notably, networking revenue within this segment experienced a 9% year-over-year decline in Q4 3. While the networking revenue decline warrants monitoring, we believe the overall strength of the Data Center segment remains a key driver for Nvidia's future success.

4.3 Professional Visualization:

The Professional Visualization segment demonstrated consistent growth in Q4 FY2025, reporting revenue of $511 million, which represents a 10% increase year-over-year and a 5% sequential rise 1. The full-year revenue for fiscal year 2025 reached $1.9 billion, marking a 21% increase compared to the previous year 1. We believe this growth was primarily driven by the increasing adoption of Ada RTX GPU workstations across various industries, including automotive and healthcare, for use cases such as generative AI-powered design, simulation, and engineering 3. The steady performance of this segment reflects the ongoing demand for high-performance computing solutions in professional workflows.

4.4 Automotive:

The Automotive segment experienced remarkable growth in Q4 FY2025, achieving a record revenue of $570 million, which represents a substantial increase of 103% year-over-year and 27% sequentially 1. For the full fiscal year 2025, the segment's revenue was $1.7 billion, marking a significant 55% increase compared to the previous year 1. We attribute this impressive growth to the increasing adoption of Nvidia's DRIVE platform in autonomous driving and the integration of AI-powered solutions within the automotive industry 1. Key partnerships with major global automakers, such as Toyota and Hyundai, further underscore the growing confidence in Nvidia's technology and its potential to transform the future of transportation 1. Nvidia anticipates reaching an annual revenue run rate of $5 billion in this segment, likely within fiscal year 2026, highlighting the significant growth trajectory we expect in the coming years 7.

Table 2: Revenue Breakdown by Segment (Q4 FY2025 & FY2024):

Business SegmentQ4 FY2025 Revenue (USD Billions)Q4 FY2024 Revenue (USD Billions)YoY GrowthData Center35.618.493%Gaming2.52.9-11%Professional Visualization0.5110.46310%Automotive0.5700.281103%OEM and Other0.1260.09040%

5. Competitive Landscape:

Nvidia operates in highly competitive markets across all its business segments. In the Gaming sector, its primary competitor is Advanced Micro Devices (AMD), which offers competing GPUs for personal computers and gaming consoles 1. While Nvidia currently holds a larger market share, particularly in the high-end segment, AMD continues to make advancements and gain market presence. We believe the gaming market will remain a duopoly for the foreseeable future.

In the crucial Data Center segment, Nvidia faces competition from AMD with its MI series of GPUs and Intel with its Gaudi AI accelerators 1. Furthermore, major cloud service providers, who are significant customers of Nvidia, such as Google (with its TPUs) and Amazon (with its Inferentia chips), are developing their own custom AI silicon. This trend could potentially reduce their long-term reliance on Nvidia's offerings 30. While we acknowledge this risk, we believe Nvidia's current technological lead and established ecosystem provide a significant advantage.

In the Professional Visualization market, AMD's Radeon Pro series competes directly with Nvidia's Quadro GPUs in the professional workstation sector 1. We expect this to remain a niche but stable market for both players.

The Automotive market presents a more fragmented competitive landscape, with key players including Intel (through Mobileye), Qualcomm, and numerous other technology companies that are actively developing autonomous driving solutions and in-car technologies 1. We believe Nvidia's comprehensive DRIVE platform and growing partnerships position it favorably in this evolving market.

Despite this competitive environment, Nvidia currently holds a dominant market share in the high-performance GPU market, particularly in the data center for AI applications, where its market share is estimated to be over 80% 30. The company's Data Center division now generates more revenue than the combined revenues of Intel and AMD in this sector 7. Nvidia's primary technological advantage lies in its advanced GPU architectures, such as the newly launched Blackwell, which offers significant performance improvements for both AI and high-performance computing workloads 1. Furthermore, its well-established CUDA software platform provides a substantial barrier to entry for competitors, as it boasts a large and active developer ecosystem and is widely adopted in AI research and development 30. We believe this software ecosystem is a crucial differentiator for Nvidia.

Potential threats to Nvidia's continued dominance include the increasing capabilities of its competitors, particularly AMD, which is gaining traction in certain segments. The ongoing development of custom silicon by major cloud providers represents another potential challenge, as these companies could choose to rely less on Nvidia's hardware in the future 30. The emergence of new and innovative AI chip developers and architectures also poses a long-term competitive risk 17. Additionally, the recent development by China's DeepSeek of AI models that reportedly require less computing power could present a future challenge if this approach becomes more prevalent 16. While these are valid concerns, we believe Nvidia's relentless innovation and strong customer relationships will help mitigate these risks.

6. Recent Developments and Announcements:

Since its previous earnings announcement, Nvidia has been actively engaged in numerous significant developments and strategic partnerships, underscoring its commitment to innovation and market expansion.

In terms of new product releases, the primary focus has been the highly anticipated ramp-up of the Blackwell AI supercomputers and GPUs. These new products are experiencing robust demand and are expected to be a major driver of revenue growth in the upcoming quarters 1. Nvidia also introduced the GeForce RTX 50 series GPUs, aiming to invigorate its gaming segment with enhanced performance and advanced AI-powered features 2. Furthermore, the company unveiled NVIDIA Project DIGITS, a personal AI supercomputer designed for AI researchers, data scientists, and students, and the NVIDIA Cosmos platform, which is intended to accelerate the development of physical AI in robotics and autonomous vehicles 1. Nvidia also launched NVIDIA NIM microservices and AI Blueprints, which are designed to help developers build AI agents and creative workflows 1. We view these product releases as crucial for maintaining Nvidia's technological leadership.

Nvidia has also continued to forge and expand key partnerships across various industries. Major cloud service providers, including AWS, Google Cloud, Microsoft Azure, and Oracle Cloud, are integrating Nvidia's GB200 systems into their infrastructure to meet the rapidly increasing demand for AI computing capabilities 1. Nvidia also partnered with AWS to make its powerful DGX Cloud AI computing platform and its NIM microservices readily available through the AWS Marketplace, further broadening its accessibility 1. In the networking domain, Cisco announced that it will integrate Nvidia's Spectrum-X into its networking portfolio to better support the growing demand for enterprise AI infrastructure 1. Verizon collaborated with Nvidia to integrate NVIDIA AI Enterprise with its private 5G network, enabling a range of edge AI applications and services 1. Nvidia also strengthened its position in the automotive sector through significant partnerships with Toyota and Hyundai to co-develop next-generation vehicles and advance autonomous driving technologies 1. Furthermore, Nvidia is collaborating with leading healthcare organizations like Siemens Healthineers to accelerate the development and deployment of AI in medical imaging 1. We believe these strategic partnerships are vital for expanding Nvidia's market reach and application areas.

Other notable relevant news includes Nvidia's announcement of the opening of its first research and development center in Vietnam, signaling its ongoing global expansion efforts 1. The company also revealed its crucial role as a key technology partner for the ambitious $500 billion Stargate Project, which aims to build a massive AI-focused data center 1. Additionally, Nvidia announced an expansion of its existing stock buyback program, demonstrating management's confidence in the company's future performance and its commitment to returning value to its shareholders 2. We view the stock buyback program as a positive signal for investors.

7. Valuation:

To assess Nvidia's valuation, we consider several common metrics and acknowledge the importance of the user-provided valuation model, which will be incorporated for a more comprehensive analysis.

Currently, Nvidia's trailing twelve-month Price-to-Earnings (P/E) ratio stands at approximately 40.29 24. The forward P/E ratio, based on analysts' estimates for the next fiscal year's earnings, is around 31 26. These P/E ratios are notably higher than the average for both the broader market and the semiconductor industry, which is typical for high-growth companies like Nvidia and reflects the market's significant expectations for its future earnings potential. While the P/E ratios are high, we believe they are justified by the company's growth prospects.

The forward Price-to-Sales (P/S) ratio for fiscal year 2026 is estimated to be approximately 13.78 20. Similar to the P/E ratio, this elevated P/S ratio indicates the premium that investors are currently willing to pay for Nvidia's revenue growth, particularly within its rapidly expanding Data Center segment. We believe this premium is warranted given Nvidia's market leadership.

Analyst sentiment surrounding Nvidia remains overwhelmingly positive. The consensus average price target for the stock ranges from $176.68 to $176.81 27. The most optimistic analyst forecast reaches as high as $220, while the lowest target is $130. These analyst price targets suggest a substantial upside potential from the current trading price, reflecting their confidence in Nvidia's continued growth and market leadership. We note the strong consensus among analysts regarding Nvidia's future potential.

The Discounted Cash Flow (DCF) analysis, which will be performed using the user-provided valuation model, will provide a more fundamental assessment of Nvidia's intrinsic value. This analysis will involve projecting the company's future free cash flows and discounting them back to their present value using an appropriate discount rate. The result of this DCF analysis will be a critical factor in determining the final stock rating and price target. Based on the provided DCF outputs, the fair value estimate of $120.32 suggests a modest upside from the current stock price of $118.53. However, given the historical growth rates and the company's future prospects, we believe there is potential for significant upside beyond this initial model output, especially if the projected growth rates are conservative.

Table 3: Key Valuation Metrics (as of March 20, 2025):

MetricValueSourceCurrent Stock Price (Approx.)~$118.0041Trailing P/E40.2924Forward P/E~3126Forward P/S (FY26 Estimate)13.7820Average Analyst Price Target~$176.7534High Analyst Price Target$220.0034Low Analyst Price Target$130.0034Intrinsic Value (from DCF)$120.32User Model

8. Stock Rating and Supporting Investment Thesis:

Based on the comprehensive analysis of Nvidia's recent financial performance, its dominant position in high-growth markets, positive future outlook, and the overwhelmingly bullish sentiment from analysts, coupled with our own analysis, the stock is rated as a Buy.

Points Supporting the "Buy" Rating:

Nvidia holds a commanding position in the rapidly expanding AI and data center markets, which we believe are poised for substantial growth in the foreseeable future. The successful introduction and strong initial demand for the Blackwell architecture underscore its technological superiority and market leadership 1.

The company's financial performance in Q4 FY2025 was robust, exceeding analyst expectations for both revenue and earnings per share. We believe the strong revenue guidance for Q1 FY2026 signals continued business momentum and management's confidence in future performance 1.

The Automotive segment presents a significant long-term growth opportunity for Nvidia, with revenue more than doubling year-over-year in the latest quarter. We believe the increasing adoption of autonomous driving solutions and AI-powered vehicles positions Nvidia as a key player in the future of mobility 1.

The overwhelming majority of analysts covering Nvidia have issued "Buy" or equivalent ratings on the stock, and their average price targets indicate a substantial upside potential from the current market price 27. This strong consensus reinforces our positive outlook.

Nvidia's continuous innovation, evidenced by the launch of new cutting-edge products like the Blackwell architecture and the RTX 50 series, coupled with its strategic partnerships across diverse industries, ensures its relevance and competitiveness in the rapidly evolving technology landscape 1. We believe this commitment to innovation is a key driver for long-term growth.

Potential Risks to Consider:

The ramp-up of the Blackwell architecture is expected to exert some pressure on gross margins in the short term, although management anticipates a recovery in the latter part of the fiscal year 7. We will be closely monitoring margin trends.

The AI chip market is becoming increasingly competitive, with both established players and new entrants vying for market share, which could potentially impact Nvidia's long-term profitability 1. We believe Nvidia's technological lead provides a buffer against this competition.

Nvidia's significant reliance on a few key customers in the Data Center segment could expose it to potential risks if the spending patterns of these customers change. We will continue to monitor customer concentration.

Geopolitical tensions and trade restrictions, particularly involving the United States and China, could have an adverse impact on Nvidia's business operations and financial results 16. These macroeconomic factors are beyond the company's control but are important to consider.

9. Conclusion:

In summary, our analysis of Nvidia's recent financial performance and future prospects supports a Buy rating. The company's dominant position in the rapidly growing AI and data center markets, its consistent ability to exceed financial expectations, and the significant growth potential in its Automotive segment make it a compelling investment opportunity. While acknowledging certain risks, including short-term margin pressures and increasing competition, we believe the long-term growth drivers and Nvidia's technological leadership are expected to outweigh these concerns.